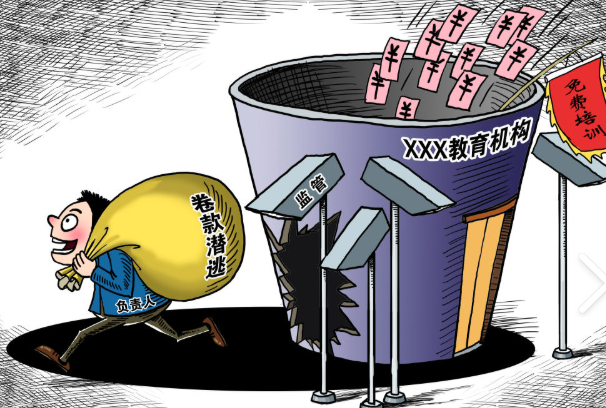

Thanks to diverse discounts and great convenience, prepaid consumption has been widely applied in service industries such as fitness, beauty and vocational training, emerging as one of the dominant consumption patterns for the public. In recent years, however, a grey industrial chain of “professional store closers” that illegally siphon off consumers’ prepaid funds has grown increasingly rampant. These perpetrators adopt a well-established fraudulent routine: taking over physical stores, collecting large amounts of prepaid deposits in a short period, and cancelling business registration to abscond with funds for illegal profits. Frequent cases of sudden store closures, uncontactable merchants and inaccessible refunds have triggered numerous rights protection disputes. Such misconduct not only infringes on citizens’ property rights, but also severely undermines public trust in the prepaid consumption sector, evolving into a prominent livelihood problem in urgent need of rectification.

Rampant Malpractices: How “Professional Store Closers” Erode Trust in Prepaid Consumption

Different from passive store closures caused by genuine operational losses, “professional store closers” aim exclusively at malicious fund embezzlement and have formed a sophisticated illegal profit model. They usually take over well-managed fitness, beauty and training stores with stable customer sources at a low cost. After replacing the legal representative and business entity, they immediately launch attractive marketing campaigns including discounted annual cards, large-quantity discounts and long-term course packages to induce consumers to make large-value top-ups and card renewals.

Once they accumulate massive prepaid funds within a short time, they suspend services under false pretexts such as store renovation and upgrading, before cancelling enterprise registration, transferring assets and completely cutting off contact with consumers. To evade legal accountability, most lawbreakers operate through shell companies and nominal legal representatives, while masterminds conceal their identities and repeat cross-regional fraudulent store closure schemes. Affected consumers are generally trapped in difficulties in evidence collection, accountability pursuit and judicial enforcement. Even if they file lawsuits to safeguard their rights, they often fail due to merchants’ insolvent status. The high cost of rights protection discourages most consumers from pursuing remedies, further fueling the spread of such malpractices.

In-depth Analysis of Root Causes: Overlapping Loopholes Trigger Chaos and Market Risks

The rampant “professional store closure” chaos results from the combined effects of industrial characteristics, regulatory deficiencies and rights protection barriers. The fitness, beauty and training sectors are asset-light industries with no substantial fixed asset restraints. Store shutdowns, entity alterations and enterprise cancellations involve simple procedures, leading to an extremely low cost for illegal fund embezzlement and abscondence. Meanwhile, the “pay-first, consume-later” nature of prepaid consumption deprives consumers of fund control, putting them in an inherently disadvantaged position.

Regulatory loopholes are the core cause of such chaos. The previous domestic regulatory system for prepaid funds was imperfect without mandatory fund escrow mechanisms, allowing merchants to freely dispose of consumers’ prepaid funds and creating opportunities for fund embezzlement and abscondence. The threshold for market entity alteration and cancellation is relatively low, and regulators lack early warning and regular supervision over stores with frequent legal representative changes and abnormal closures, making it impossible to prevent risks in advance. In terms of rights protection, most consumers lack legal awareness, fail to preserve standardized contracts and consumption vouchers, and are deterred by the low individual dispute value and the time-consuming, costly nature of individual litigation.

Such malpractices bring extensive adverse impacts. For consumers, prepaid fund losses greatly diminish consumption security and sense of trust. For the industry, individual malicious abscondence incidents trigger widespread public trust crises in the entire service sector, bringing collateral losses to law-abiding operators. For society, massive backlogged consumption disputes waste administrative and judicial resources, easily trigger group rights protection incidents, and disrupt market order and social stability.

Comprehensive Governance: Institutional Safeguards and Targeted Regulation Drive Industrial Standardization

To address prominent problems including “professional store closures” and refund difficulties in the prepaid card sector, national and local authorities have continuously improved regulatory systems and intensified rectification efforts, building a comprehensive governance framework featuring source prevention, whole-process supervision and strict accountability. The judicial interpretation on civil disputes of prepaid consumption, implemented in May 2025, has consolidated the legal bottom line. It clarifies that operators who maliciously close stores and abscond with funds shall bear punitive compensation liabilities, and those suspected of criminal offenses will be transferred for legal investigation, substantially raising the cost of illegal conduct.

Local authorities have rolled out refined regulatory measures. Regions including Beijing and Shanghai have implemented prepaid card filing and publicity systems as well as special prepaid fund escrow mechanisms to ensure earmarked fund use and dynamic supervision, fundamentally curbing merchants’ illegal fund misappropriation and abscondence. Meanwhile, a credit supervision system has been established to blacklist individuals responsible for malicious store closures and refund refusals, imposing joint penalties such as credit restraints and industry entry bans to cut off cross-regional repeated illegal chains.

In addition, market supervision departments, consumer associations and courts have jointly built an integrated dispute resolution platform, adopting collective mediation and expedited case filing mechanisms to simplify rights protection procedures and reduce public litigation costs. Targeted special rectification campaigns have been continuously launched to investigate behind-the-scenes criminal gangs of professional store closers and severely punish illegal acts including false operation and malicious fund embezzlement, realizing a shift from passive dispute settlement to active risk prevention.

Driven by the three-fold governance mechanism of legal restraint, fund supervision and credit discipline, the unregulated and disorderly development of the prepaid consumption industry has been effectively curbed. With the continuous improvement of the regulatory system in the future, the living space for “professional store closers” will be completely eliminated. The prepaid card consumption industry will gradually achieve standardization and transparency, effectively protecting consumers’ legitimate rights and interests and steadily boosting consumer market confidence.